Recent data centres events and conferences have centered around the net zero agenda; the journey data centre clients are taking to achieve net zero today and what the future will look like to get there.

Pre-COVID, the data centre sector growth was exponential. Post-COVID, our sector has exploded with Gartner predicting data centre spend estimated to hit $200bn by the end of the year and with it comes our responsibility as an industry to create a sector that treads as lightly on our planet as it can. The pull towards net zero is coming from providers and investors with 75% of investment executives agreeing that a company’s sustainability performance is important when making investment decisions while the push is coming from the supply chain and regulators propelling the industry towards green data centres requirements. We also all know how many steps have already been taken in our industry to help negate this footprint and greening our data centres with greater efficiency initiatives such as using renewable energy, strategies such as cooling racks rather than whole buildings and by undertaking whole life carbon assessments at design and build stage. And many providers in our sector have also been the earliest and the biggest funders of green energy with wind farms and re-forestation of areas.

At RLB we too have been working to support our clients, both in the data centre sector and across other areas of the built environment, towards their net zero ambition, especially in relation to reducing their Nitrogen Oxide emission (NOx) rates. Creating a NOx calculator we are able to identify the cost impact of NOx emissions for our clients and by using a sliding scale, the tool shows how much it would cost to add or reduce the amount of kilograms of NOx on a project. The results then guide us to assess whether the project schedule will be prolonged or shortened in relation to the associated NOx emission cap per country.

However, as we move closer in our journey of looking at how the data centre sector can achieve carbon zero or even carbon negative, as providers such as Microsoft has committed to becoming by 2030, we need to look at beyond the case for net zero. We need to align the environmental impact of our data centres into the wider view of elements to consider when designing and building data centres and if carbon zero is to be prioritised the effect this will have on other areas of a project’s lifecycle and cost.

We are working with clients to take this holistic approach across many of the sectors we work in – be it building new data centres within Europe or looking how we support clients with re-purposing of existing infrastructure, such as within healthcare estate in the UK. This approach considers how clients design and build or refurbish their projects looking at how they minimise the impact of these builds on the environment, reduce their carbon footprint and look to build for a green future.

But it also puts this into the context of other variables, with a more holistic outcomes approach rather than one based on just scope or specifications.

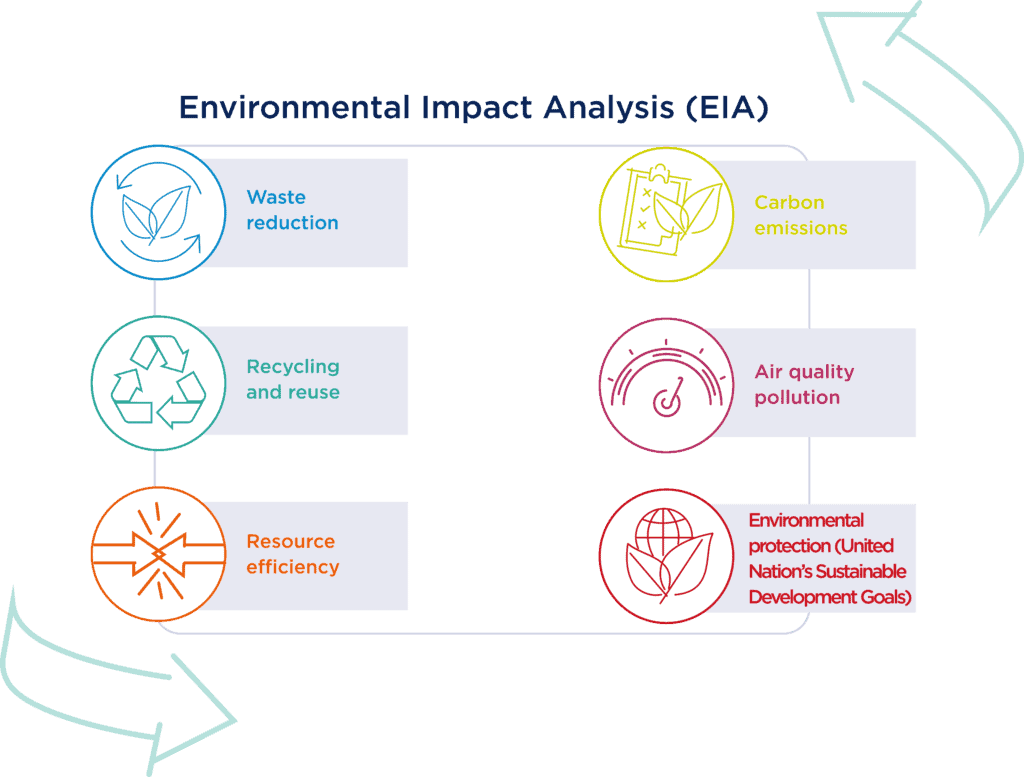

Not only evaluating what the Environmental Impact Analysis (EIA) of each data centre project will be by its:

But also looking at Cost Benefit Analysis (CBA) using measures such as the UK’s HM Treasury Unit Cost Database to identify fiscal and economic savings to public services and taxpayers.

Assessing what is the Economic Impact Analysis (EIA) using Local Economic Multipliers (LM3) and spending proxies to understand how your project contributes to the local economy and supports local economic growth.

Analysing what is the Gross Value Added (GVA) uplift will entail using Eurostat and the Office of National Statistics data to understand the indirect and induced effects of direct employment and productivity.

And estimating what is the Social Return on Investment (SROI) the sum of fiscal, economic, environmental and social value will be by combined CBA, SVA and EIA to calculate the SROI.

Our team is working closely with many clients both in the public sector and the private sector and with our supply chain to ensure these variables are considered to bring real life cost and lifetime cost into equation. There is no doubt we need to work towards a net zero, or net negative data centre world – one that supports the new world we now live in, where the need for data, and data centres, will continue to increase, but one that nurtures this world. However, as we work to understand how we continue our journey of net zero for the data centre arena, we need to contextualise it and understand the other factors that are at play.

FURTHER INFORMATION: